Why does fragmented sustainability data matter? It raises audit costs, increases compliance risks, and weakens decision-making. For leaders, this hidden cost appears when reporting stalls, audits flag risks, or compliance penalties hit.

The issue of fragmented sustainability data is urgent in 2026. A perfect storm is forming. Strict EU CSRD mandates have arrived. Sustainability reporting demands unified, audit-ready datasets. The standard matches the rigor of a financial audit, yet many still use spreadsheets and disconnected systems.

Legacy quick fixes create inconsistent ESG data and slow reporting. It also weakens financial performance.

The link between sustainability results and financial outcomes breaks. What was once a routine reporting is now a strategic risk. New regulations are not the sole cause. These challenges stem from years of underinvestment in data infrastructure.

When companies delay strengthening foundations, long-term competitive advantage erodes with each year of inaction.

Fragmented data: The root cause of inconsistent ESG reporting

KPMG’s report, Managing sustainability data in 2025, identifies fragmented data as the top obstacle to reliable reporting.

Large companies work with data from multiple sources. These include ERP and HR systems, procurement tools, supplier reports, spreadsheets, and third‑party platforms.

While data may be accurate in isolation, the challenge arises when it must be consolidated, mapped across multiple standards, and explained consistently to regulators, auditors, and stakeholders.

We have worked with organizations where:

- Scope 3 emissions figures differed depending on whether they were pulled for CSRD, CDP, or for internal purposes.

- Supplier data was manually reclassified every reporting cycle because historical mappings were never standardized.

- Local teams maintained their own calculation logic, making data consolidation more complicated than expected.

Fragmentation grows as organizations try to meet many overlapping rules. These include the Sustainability Reporting Directive (CSRD), ESRS, CDP, EcoVadis, PPWR, EPR, and various local regulations. This is especially true under the CSRD across the European Union. What began as a practical workaround quickly became a permanent structure and, as a result, a structural weakness.

Over time, sustainability teams spend more energy fixing data mistakes than using the insights. Deloitte’s 2024 Sustainability Action Report shows that fragmented data is the biggest barrier to ESG reporting. 57–88% of executives identified data quality as a major concern.

This mistrust prevents teams from using the data for real planning. Instead of helping with scenario analysis, these efforts fall short. They also do not link results to revenue and costs. They stay stuck in basic compliance. Without trust, teams are unable to make informed decisions with a comprehensive view of performance.

The hidden cost of manual ESG reporting

Many companies rely too heavily on disconnected spreadsheets. Skilled analysts spend most of their time collecting and cleaning data, leaving little time for real strategic work. Teams manually copy figures between frameworks, adjust calculations, and resolve inconsistencies under time pressure. The underlying data collection approach has never scaled across the business and supply chain.

We have seen:

- Manual checks delayed reporting by months because teams could not resolve them easily.

- External advisors repeatedly came to “validate” numbers that should already be validated.

- Senior leaders pulled into last-minute review cycles because confidence in the data was too low.

The “manual labor tax” is rarely budgeted but is significant. Teams stuck doing cleanup lose the ability to act quickly. They have less time to improve their work, follow new rules, or use ESG‑related opportunities.

Increased regulatory and assurance risk

Auditors approach sustainability data in the same way they approach financial reporting. They expect clear data ownership and documented methodologies. With data scattered across tools and spreadsheets, meeting these expectations becomes difficult.

Teams rely on manual explanations rather than systematic evidence. This increases the likelihood of delays or qualified opinions. In this context, fragmentation undermines confidence. This is not only for auditors but for executives signing off on disclosures.

We have supported organizations where:

- Teams could only answer audit questions by tracking individuals rather than referencing systems.

- Teams failed to document method changes, which led to differences from year to year.

- Leaders were uncomfortable signing off on disclosures because confidence in the underlying data was low.

Audits become more stressful and take more time. Unexpected issues and rework are common. This is not because teams lack skill. Teams never built the data foundation for this level of scrutiny.

Why technology alone does not provide ESG data integration

Adding another tool rarely fixes fragmentation. It often increases it. But large companies already keep data on many disconnected platforms, which only makes the problem worse.

PwC’s 2025 Global Sustainability Reporting Survey finds that 87% of companies still use spreadsheets. It warns that without data integration the same challenges continue.

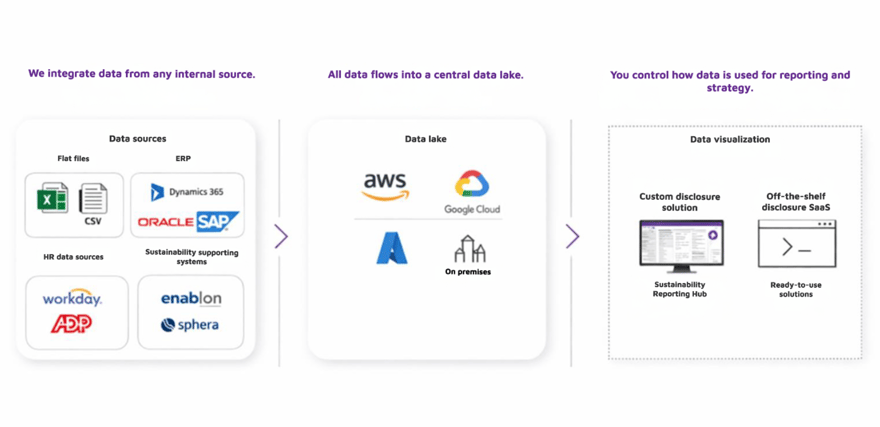

The core issue is not the lack of tools. The lack of a unified data foundation treats ESG data as enterprise data. An integrated approach does not require replacing existing systems.

Instead, it connects them through a structured data layer designed for sustainability requirements. Data integration tools often power these layers and automate data validation, transformation, and lineage.

What leading organizations are doing differently

Most mature companies are moving away from quick fixes and towards data platforms that:

- Consolidate sources without replacing legacy systems.

- Support multiple frameworks from a single data model.

- Embed governance, clear ownership, and auditability

- Enable real-time monitoring and strategic decision-making.

When organizations finally address years of ad hoc implementations and inconsistent standards, the shift is immediate:

- Reporting cycles shorten.

- Confidence in the data improves.

- Teams move from reconciliation to analysis.

- ESG data starts informing real decisions.

This shift reflects a broader change. Corporate sustainability reporting is beginning to resemble financial reporting in its expectations and discipline.

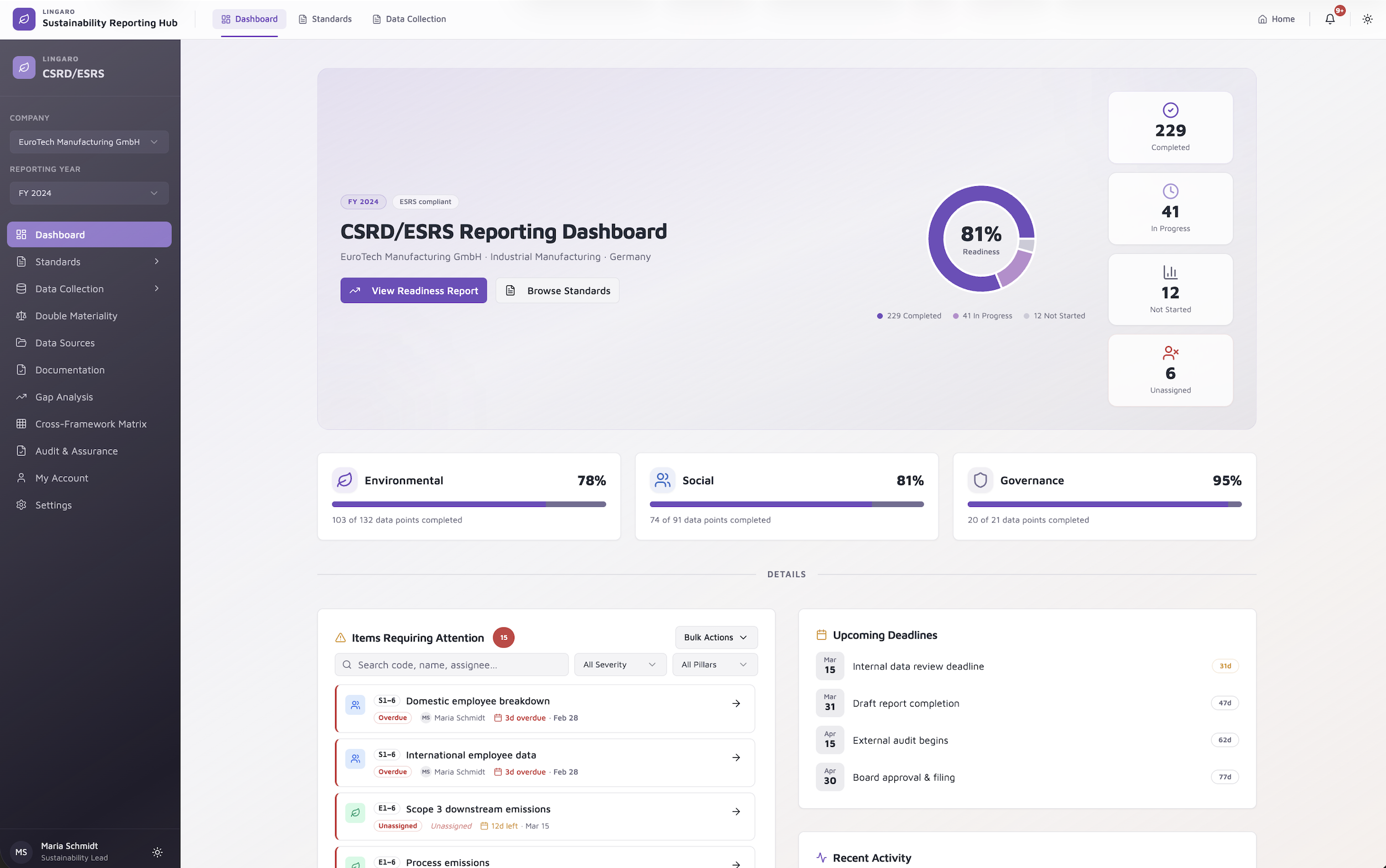

How Lingaro can support you with this transformation

Lingaro has the Sustainability Reporting Hub, a centralized, client‑owned data foundation that connects your systems, workflows, and reporting frameworks.

Compliance is no longer enough; transparency is now a performance driver. It stays ready for assurance and supports both reporting and decisions.

In See the Strategic Pathways to Data-Driven Sustainability, we noted that this data rarely serves one purpose. It works best when teams manage it with a strategic approach.

|

Current state (As-Is) |

Our approach |

|

Automated SharePoint uploads |

API based integrations with source systems for reliable, scalable data ingestion |

|

Manual data checks and reconciliations |

Automated validation rules and consistency checks at ingestion and consolidation |

|

Limited or lacking version control |

Data historization and full audit trails with change tracking |

|

Siloed data with limited transparency |

Centralized sustainability data lake connected to executive dashboards |

|

Spreadsheet-driven consolidation |

Standardized data models reusable across frameworks and reports |

|

Late-stage data corrections |

Upstream controls to identify issues early in the reporting cycle |

Once the robust data foundation is in place, you can:

- Build a custom solution tailored to your specific regulatory, operational, and strategic needs.

- Connect off-the-shelf SaaS tools for reporting, disclosures, or specific use cases.

Both approaches are effective when built on a common, governed data layer.

Concluding thoughts

Simple compliance is no longer enough; it is merely the baseline. Companies that use sustainability data in the same way they use financial data will grow and gain an edge.

The organizations struggling today are paying the price for past choices. They delayed integration, relied on old spreadsheets, and treated ESG data as a short-term task. This fragmentation inevitably leads to delayed audits, stalled strategies, and lost opportunities.

Lingaro helps you break this cycle. By building a client-owned data estate, we turn your sustainability data into a permanent strategic asset. This lets you move past the limits of standard “black box” tools. It helps you track performance, find AI-driven cost savings.

Building an audit-ready, scalable data infrastructure is no longer a technical preference. It has become a fundamental leadership requirement. In 2026, the market will split between companies that only report data and those that use it to drive real change.

In 2026, sustainability reporting requires unified, audit ready data sets. Fragmented spreadsheets increase the risk of delays, inconsistencies, and compliance pressure. Lingaro supports organizations in building centralized, client owned sustainability data foundations designed for reporting, audit, and long-term performance management.

With this approach, sustainability data stops acting as a reporting burden and starts working as a strategic asset. Build an audit ready, scalable data foundation and move from fragmented spreadsheets to unified, decision ready insight.

FAQ

What is ESG data?

ESG data captures key metrics used in environmental, social, and governance (ESG) reporting. These include among others: emissions, workforce indicators, and governance practices.

What does data integration mean in sustainability reporting?

Data integration connects data from multiple sources into a governed layer enabling teams to get a comprehensive view.

Why is CSRD driving new reporting requirements?

The corporate sustainability reporting directive (CSRD) increases reporting requirements for the biggest companies operating in the European Union, including stronger assurance expectations.

What are data integration tools used for?

Data integration tools help automate data ingestion, validation, mapping, and lineage; reducing manual effort and improving consistency.

How does sustainability reporting link to financial performance?

Reliable sustainability reporting supports better forecasting and risk management and can connect outcomes to financial performance and strategy.

What reporting frameworks might companies align to?

Many organizations map disclosures to mandatory reporting framework such as ESRS, ISSB and, where relevant, voluntary frameworks such as CDP, GRI, SASB and others.

%20article%20%E2%80%93%20blog%20coversdesktop.jpg?width=1200&height=712&name=2298%20Life%20Cycle%20Assessment%20(LCA)%20article%20%E2%80%93%20blog%20coversdesktop.jpg)